LISTEN TO EP.99

EP.99 DESCRIPTION

The Financial Questions You Should Be Asking During a Recession

Have you been wondering if we are truly in a recession and how you should prepare? Gil Baumgarten, one of the nation’s top financial advisors, Founder, and President of Segment Wealth Management, answers this question and others as he shares how to establish good habits when handling your assets. Hear his perspective on long-term investments both for return and stability, the number one financial mistake investors should avoid, and healthy habits to put into practice. Baumgarten reminds us that the Bible does not say that money itself is evil. Rather, the love of money is evil and some of the rich were only vilified because of their motives. Learn principles of good stewardship and how money can be used to heal, help and educate when properly managed.

Disclosure: The Podcast discussion represents neither an attorney nor an accountant, and no portion of the podcast content should be interpreted as legal, accounting, or tax advice. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). These are general tips and not meant to be personalized financial advice to your unique situation

EP.99 TRANSCRIPT

Introduction

Welcome to the influencers podcast. I’m Scott Young with cohost Dave Donaldson, who is traveling the world, influencing people, he’s out on assignment today, but we’re glad that you are with us. Let me ask you a question. Have you done anything with money today? And if not today, probably in the last few days, money helps us. In some ways measure the value of life. It can be connected to many of life’s problems. It can be if misplaced the root of evil, but it also, if properly handled can be a tool to help us heal, help and educate. Gil Baumgarten is one of the nation’s top financial advisors. He is the founder and president of Segment Wealth Management. And since its inception in 2010, it has grown to be one of the top 10 firms in Houston. It has over a billion dollars in client assets under advisement. Gil is also a nine time recipient of the Top Financial Advisors Distinction. He is ranked among the 35 best advisors in Texas by Barron’s, but it’s not just money in Gil’s life. He is an outdoorsman. He loves to hunt. He loves to fish. He excels in sports and interestingly he is his university’s billiard champion. He’s an award-winning woodworker. He loves his family, his friends, and his colleagues and Gil. I wanna welcome you to The Influencers Podcast and, and just let me start by asking how do you become your university’s billiard champion?

Well, it was once said that being good at pool is evidence of a misspent youth. So maybe I, maybe I just played too much pool when I was growing up as a kid, but I like anything that’s precise. And so archery, dart, marksmanship, skeet and all of those sports I love. And so anyhow, I like to play pool and ran my campus pool hall when I was in college and hustled a few games on the side. So,

And you, what university, where did you go to school? Where did you take education?

I went, I went to the metropolis of Nacogdoches, Texas and went to Steven F. Austin State University.

Are We in a Recession?

Well, we’re glad that you’re with us today and we’re gonna talk about finances. There’s a, a really a burning question. As of the recording of this episode with the GDP being down the last two quarters rising inflation interest rates are up. I, I have friends that have been looking for a house lately and they’re really filling the pinch. People have labeled this economic time we’re in as a transition or a, a downturn some call it a recession. Wanna get your insight on it. What do you think’s really happening in the economy today? Gil?

Well, you got a lot of cross currents. The stock market has had a, you know, four or five year run, really a 10 year run to the culmination of this recent peak that we had, you know, you had COVID debt market down draft 30% in March of 2020, which it recovered from and suddenly doubled in market value, low interest rates drive a premium in stock prices because people don’t have any other good alternatives. And so the specter of hope for higher stock prices is probably squelched a little bit by higher interest rates that give them other alternatives. I mean a CD one year CD a year ago, would’ve yielded a 10th of a percent. Now it yields 20 times that so people are more incentivized to sell their stocks and buy safer things that might offer them some type of a fixed return where stocks never offer you a fixed return and much to your benefit because they tend to go up a whole lot more than they go down. So I think that’s, what’s happening with sending some shivers through the stock market, with rising interest rates and inflation that supports those rising interest rates.

Would you go so far, would you use the word “recession” or there seems to be a hesitancy to using that word? Maybe you can explain why that is and just, can we use that word or do we not use it yet? Just your…

I, I would use it. The reason why it’s not a preferred term is that’s a political issue. If somebody else had been in office the opposite team would been calling the recession word all over them. And so it’s just a matter of who’s in power and who controls the narrative. So recession is a bad word for somebody in charge, unless they can blame somebody else for it. And, and that’s even been attempted this time around. So yeah, I think we’re in a, I think we’re in the beginning of a recession and, you know, the last oh nine recessions that we have had have come with, what’s called an inverted yield curve. And that’s where people demand a higher rate of return for their short term deposits than they require of their long term deposits. Most often, if you’re looking at a 30 year instrument, it carries greater risks to the investor and therefore requires a higher rate of return to be compensated for that in an inverted yield curve.

If you were to plot along a one year three year, five year, 10 30 year security, you would expect there to be an upward sloping to the right curve that’s required, but inverted yield curve, it’s downward sloping to the right where people demand a higher rate of return for the short deposits because of what their expectations were for the economy and the future. We have an inverted yield curve today. And so that’s been a precursor to pretty much every recession we’ve ever had. Now I will say we’ve had more inverted yield curves than we have had recessions. So it is not 100%, three out of the last 13 inverted yield curve. Occurrences did not result in a recession. This could be the fourth. So I don’t know the answer to that, but I would say to be careful.

Can You Bulletproof Your Finances?

So we have people that are listening. They want to be wise with their finances. I, is there any way to be Bulletproof in a, an economy like this, or you just make the best guess as you can, or listen to the best advice you can.

There are ways to Bulletproof yourself, but that in fact comes as a downside too. The first thing is you would have to liquidate the securities that you already owned, which would result in taxes. If you had profits on those securities, then you would have to be correct about the call that you made, that the vehicles that you sold actually did worse than the vehicles that you bought. So you could be Bulletproof by buying a treasury bill or a CD or a money fund, or some type of short term instrument with a guaranteed short, small interest rate. Then if you had miscalculated at like, you might have done three weeks ago and the stock market jumped 10%, while you went to cash, it’s gonna take four years of your CD return to equate to what you would’ve made in the last three weeks in the stock market. So it’s a, it’s a dicey game. So if you want to guarantee, you can get a guarantee, but in many cases, the no guarantee would’ve been the better bet.

Now you’ve been giving financial advice for how many years,

38 years.

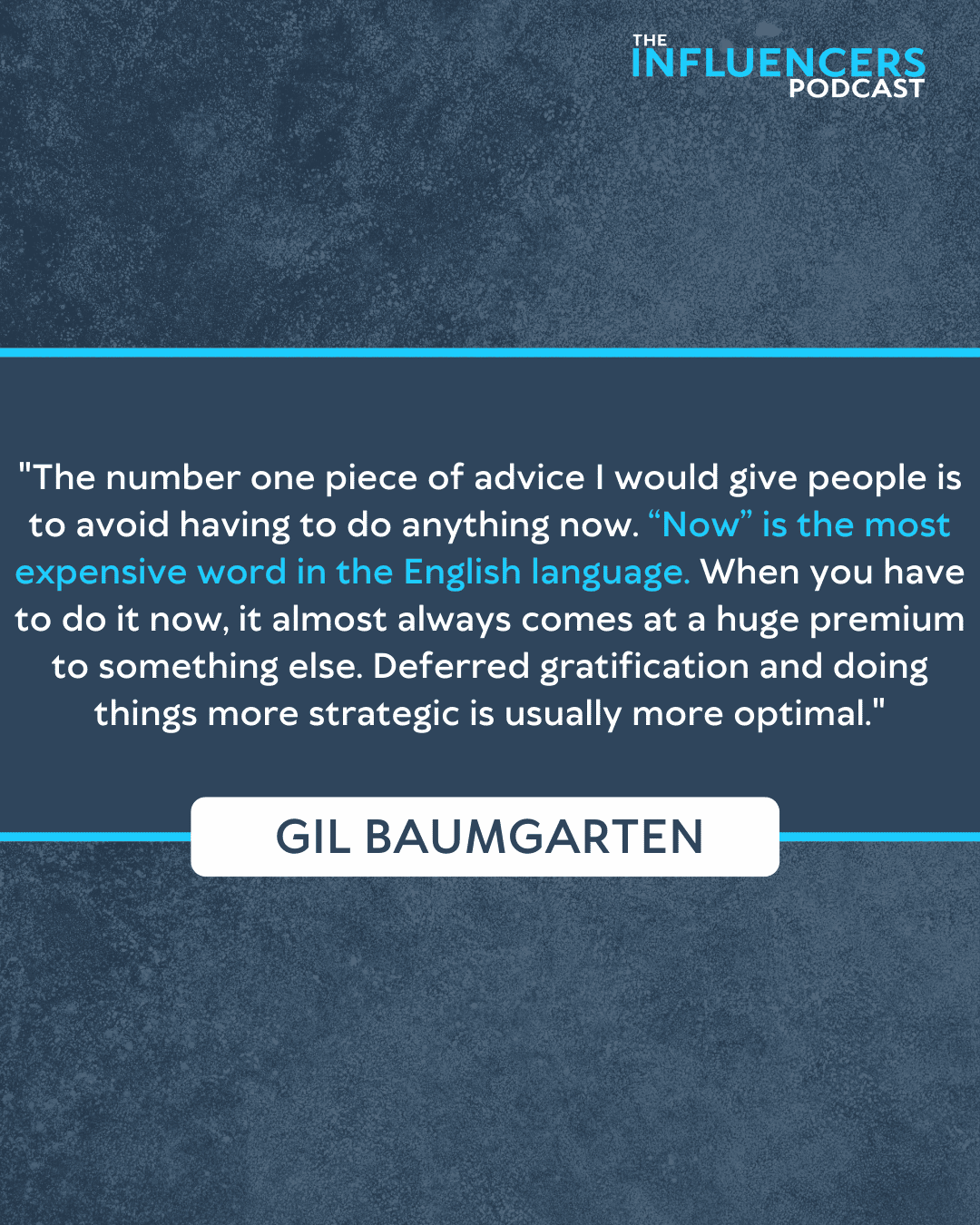

The Most Expensive Word in the English Language

So you’ve seen some cycles and you mentioned some of the cycles we’ve been through, what are some of the huge mistakes that people make in uncertain times like we are in now and, and hopefully to advise people to avoid these type of mistakes?

Well, the number one piece of advice that I would give people is to avoid having to do anything now. “Now” is the most expensive word in the English language, when it comes to investments we have seen people who want to buy a house. Now they wanna buy a new car. Now they want to de-risk their portfolio because they’ve just lost money and they want to do it now. So when you have to do it now that almost always comes at a huge premium of something else. And so deferred gratification and doing things more strategic could be more optimal. We’ve had a conversation recently with a, not a client, but a friend who had recently inherited some money. Most of which in the came in the form of a IRA and dad’s IRA had pending tax liability, and this person wanted to buy a house and they wanted to buy it now. So they liquidated dad’s IRA and paid far more in tax than they would have if they would’ve liquidated the IRA over, say a three or four year time period, but they wanted the money now. And that being the case, they probably end up paying end up, paid close to $50,000 in taxes, more than they would’ve been. If they simply could have waited a couple of years to have liquidated the IRA. So avoid now.

So is this the time that we put money in the market slowly dollar cost average. So when you say not doing it, now we have to do something without money. Well,

Demystifying the Stock Market

Yeah. Yeah. So let’s just to give people a little bit of historical perspective. People view the stock market as this random thing. That just seems like a huge bet. And it’s, it’s really not that random in 81% of all 12 month time periods for the last three generations, the stock market generated a positive rate of return. That’s not randomness. If it was random, it would be 50, 50, 80 1%. If you were to drop your money into any month for the past 75 years, and look at the forward return 12 months after that, you would’ve had a positive return in 81% of all circumstances that doesn’t make mean you’re gonna make money all the time. That doesn’t mean that that 19% of the time wouldn’t scare you to death. But the reality is that stocks accumulate value over time. And there’s significant tax incentive to staying long term invested a deferred tax that you might have had a profit 10 years ago and never sold that vehicle.

It’s not taxed until you sell it. And if you’ve waited 10 years or 20 or 30 years to sell that vehicle, you’re earning return on top of return that can compound to a 25% higher rate of return than the stock market provides in the stock market has provided a 9% rate of return that goes back generations. So you’re really talking about a, an 11% rate of return if it’s compounded and oh, by the way, any stock or real estate asset that’s held individually until death is tax free to whoever inherits it other than estate taxes. And you’d have to exceed 24 million between two spouses for that to be a problem. So many people don’t understand that a deferred gain is tax free. When you inherit some from someone else, we had a client who died in 2017 with a $19 million portfolio with 7.5 million of unrealized gain that’s gain of increase in market value that had never been sold.

That was tax free to the surviving spouse. And when that spouse dies, it’ll be tax free again to the kids. So these are profits that dad might have earned in 1973 or 1984, or sometime in the past completely tax exempt at the death of the first spouse. And so that right there, which should reset most everybody’s expectations about what proper, proper investing methodology should include. It should include a low transaction methodology, probably Contra to what a broker might recommend because they like transactional methodologies. They want to charge fees for the things that they provide. They want people to buy and sell, which has significant tax deterioration with regard to how it would unfold in a client’s actual account.

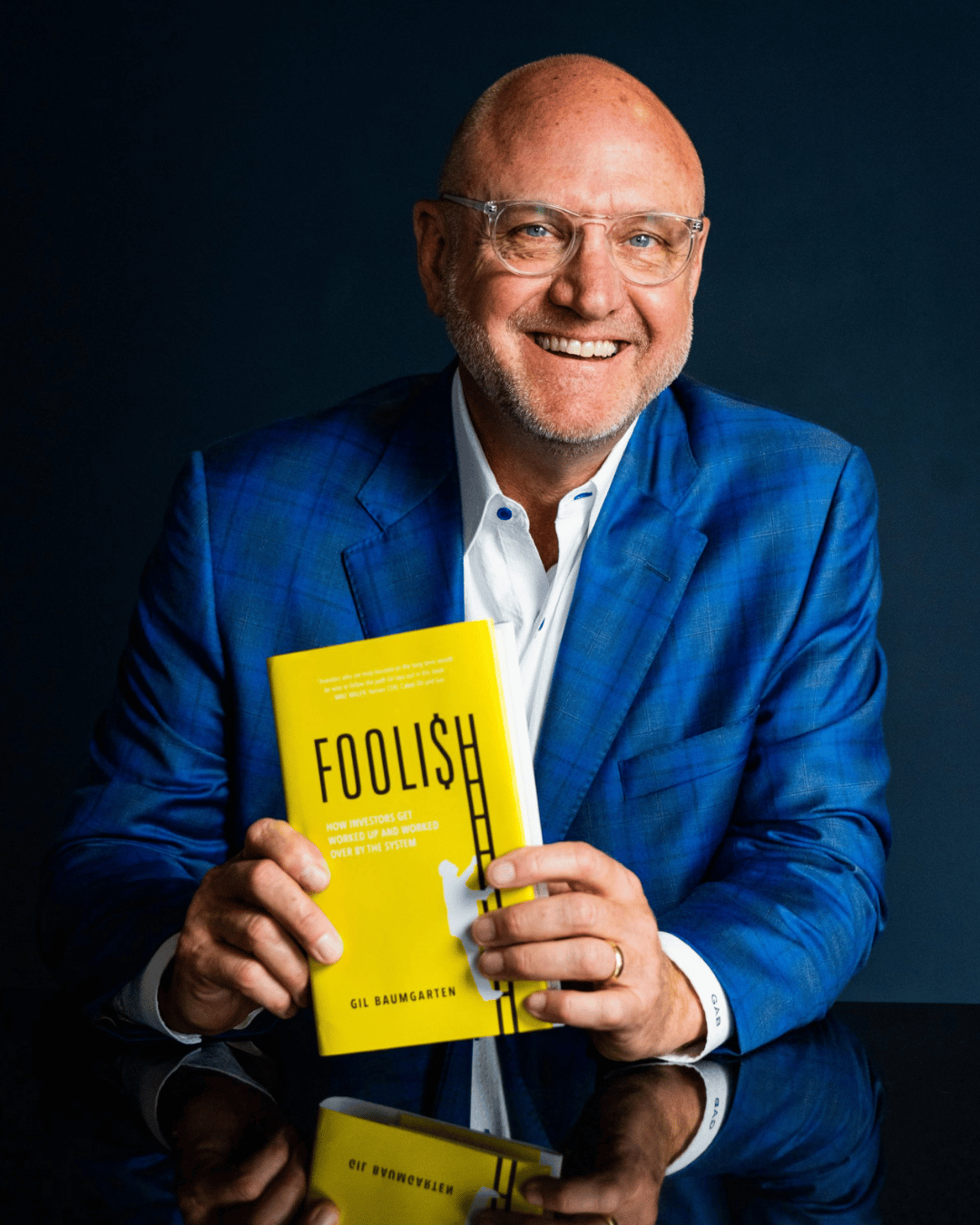

So that was such good advice. And if you’re listening to, there are people that have assets that are listening, that are wondering how they can best give them to the next generation. There’s gonna be a huge transfer of wealth. I, I know you have a book. People will be trying to get some wisdom. This is great material. You have a new book that’s out called Foolish, which is an interesting title. It’s about how investors get worked up and worked over by the system when they read that, will they get this kind of advice that you’re sharing with us today? Gil?

Going Behind the Scenes

Absolutely. The first third of the book is how the brokerage business operates what the legal confines are of the type of advice that they give. What kind of culpability an advisor in the brokerage community has what kind of leeway and latitude he, or she would have with regard to advice and conflicted advice in particular, the dark corners that they make money in, that you would not believe or really understand unless it was being explained to you in this way. And so that’s the reason why I got out of the brokerage business. The stakes just got too high for me. Once I learned, once I learned how the sausage was made, I figured I needed to exit the brokerage business and then switch to a fiduciary platform where my allegiances to the client was a requirement. And so that journey has been sort of laid out in my book.

So the first third of the book is about the brokerage industry and how it operates in the back. Two thirds is about people and how they make decisions, how they justify, how they self justify idolatry issues that they have with money. A non-stewardship mentality that’s prevalent in the world today. And that kind of permeates how we do things, ego and how our ego gets affirmed in, in speculative investments versus regular investments. And I make the distinction between a speculation, which is really how most people invest. They swap from Bitcoin to AMC theater stock, to Tesla stock, to whatever. And those are really just a string of speculations. They are not investments. So that self justification feeds our ego need to need to be affirmed so that we can have bragging rights with our friends and top them. When they’re up on the putting green bragging about, you know, how they made 10 times the their money in some stock, they’re not telling you that they lost 10 times their money in, you know, 50 other things. And so those, those are the kind of things that we drill down into to help people establish better habits of the way they, you know, look to their money for affirmation.

Fiduciary… What It’s Important

You’ll give such good advice. And if you are just want to ask yourself a question friends it’s is the person that’s advising you fiduciary or not. Do they have responsibility to you or not? That’s a great question to ask, as you consider handling your own assets if people today influencers that are listening to the podcast, have some long-term goals for return and stability, what kind of investments would you say they should be looking at?

Well, let’s back up for a second and discuss what you just said about fiduciary. Yeah, sure. It’s so convoluted and because of the rules of engagement and the way the regulations are with regard to how a broker versus an advisor has to communicate with clients. There are a couple of questions that you can ask. That’ll cut through a lot of the fluff of the way they are going to respond to you. And so, because the brokerage business is under scrutiny from the SEC and from FINRA, they’ve responded with a false flag, in my opinion, with this new regulatory reform that passed last year called regulation, best interest reg BI and the brokers will quote that as though they now have your best interest in mind, but what you would find if you read regulation best interest, is that it is not a best interest requirement.

It ultimately requires on disclosure, which is not the same thing as fiduciary. And so I would call it sort of fiduciary light. And so here is a question that you can ask your advisor, that their response will determine whether they are a fiduciary or whether they are not ask them simply if they receive 12 B, one commissions, if they receive 12 B, one commissions, they cannot be a fiduciary. And with the yes or no response to whether they receive 12 B, one commissions or not will be all you need to know as to whether they have to look out for you or whether they don’t have to look out for you. A 12 BK commission is a kickback that’s built inside of the fee structure of a mutual fund. A fiduciary can never accept under any circumstances, a 12 BKK commission and a non fiduciary most likely will be receiving 12 B, one kickback commission. So that would be the easiest way to ask that question rather than say, are you a fiduciary will a bro, a broker is going to respond in all of the ways that he can act as a fiduciary, but he’s not going to tell you about the ways that he does not have to act like a fiduciary. And so the 12 BKK question is a real easy way to cut through the weeds.

Gil, that was worth the price of admission right there. That one question 12 B one commission. That’s a great question. Thank you for sharing with us now back to people that are looking for some long term stability, long term returns, not just thinking about now, but stretching out few years, what kind of things should we be looking at.

Low Stress Investing

Pre diversified baskets of securities, such as a mutual fund or an ETF ex exceptional ways for investors to participate because it’s sort of a mindless investment. It can under certain circumstances relieve the burden of what should I be doing next? That is the, that’s the burden that any investor who manages their own money has to bear. And that is the constant nagging question about what should I be doing next? When you that’s the primary value of an advisor, you make it their problem to do for you, what should be done next? That, and that’s the reason why you really should be hiring a fiduciary and not a broker. But that nagging question is many times minimized by buying a pre diversified basket. So if you’re buying a mutual fund, that’s investing in the stock market, it might have 200 securities in it. There are ETFs that exist, which is another version of a mutual fund and lower cost and lower tax.

So I’m going to recommend an ETF over a mutual fund. For those two reasons. Some of them have 3000 securities in them. When you think about it, that way 3000 securities, whether Tesla is good or bad, or whether at and T is good or bad, it’s completely irrelevant to the whole equation. It means that the 81% is probably going to apply to you. And therefore it eliminates the decision of what you have to do next. You don’t even have to worry about doing something next, you do that and you hold it over a long time. Period is a very high odds, likelihood that you’re gonna make money from that. And you’re gonna have a low cost and low tax outcome from not selling it. And an ETF is taxed differently than a mutual fund, a traditional open and mutual fund like you would get from fidelity or most, mostly from American funds or Dryfus.

Two of those companies are also in the ETF business. Fidelity is not those ETFs have a lower cost structure and generally, and they have a lower tax structure and open-ended mutual fund has co-mingled accounting. That means that the activity of other investors drives taxable activity for every investor. An ETF does not have co-mingled accounting. That means that every share of an ETF that an investor owns is taxed only based on the activity of that investor, not the activity of other investors that compounds over 10, 20, 30 years to generate significantly lower taxes on an ETF than an identical mutual fund, just from a structural perspective. So a large diversified ETF Vanguard in particular is extremely low cost because Vanguard is not a for-profit business. Vanguard is run as a co-op. So it’s a shared expense type of arrangement. Every other mutual fund company that I know of has a for-profit motive and therefore the fees are a lot higher. So I’m gonna direct people towards Vanguard and Vanguard ETFs very quickly. When I, when you ask the question about the types of diversified vehicles that allow people to build with wealth without a lot of worry or risk.

How the Bible Views Wealth

Now we’re here on the influencers podcast, because we would like to see people increase in the influencer of their life to change their world. And the greater world we live in mismanage money creates so much problem in homes. It’s one of the number one breakup points of homes, anxiety, intentions, our audience I, myself and a lot of our audience are people of faith. And so I’m just wondering Gil, you’re a man of faith and how these two worlds collide the material and the spiritual your, your faith in the finances, your heart and your treasure. How do these two worlds kind of come together as you try to help people increase the influence of their life?

You know, in the Bible, we have numerous examples about love, love, and money being discussed and entrepreneurs and business people were rarely vilified in the Bible. The money changers were vilified because they were applying their trade in the temples in the church. The tax collectors were vilified because for the most part, they were not truthful dealers. The rich were vilified only for their lack of generosity and not because they were merely rich. And despite popular recitation about money being the root of all evil, it was actually the love of money that was listed as the root of all evil. So I don’t find the biblical principle to be in conflict with a profit motive. And if you look at the parable of the talents, the master castigated the one who buried his talents and didn’t use them. And he exalted the ones that actually did something and took risks with the talents that were given to them. And I think that there’s absolutely no problem with capitalism, from an honorable and straightforward perspective. It’s slide dealing, it’s the side arrangements. It’s those kind of things that I think are inconsistent with biblical virtues and values, but I think capitalism executed that way is 100% consistent with biblical values.

What a joy just have, you are a fountain of wisdom and knowledge, and I I’m, I’ve taken notes down here. Some things I’m gonna be asking about, you do wanna put in our show notes for those that want to connect the websites to get a hold of Gil. The book that he’s written Foolish, How Investors Get Worked Up and Worked Over by the System and how you can avoid that and how you can be successful, which I, I think that money handled well, does that Gil? I wanna thank you just for being a part of The Influencers Podcast. We have appreciated your time and just the expertise that you’ve shared with us today. Thank you so very much

Happy to do it. Thanks for having me

For The Influencers Podcast. I’m Scott Young, until we talk to you next time, keep changing your world. Be an influencer and let your world be changed. And the world you live in be changed.

Listen

to past episodes

Your Guide

to being a church that meets community needs

We want to hear

from you!